Author: Evan Dawe

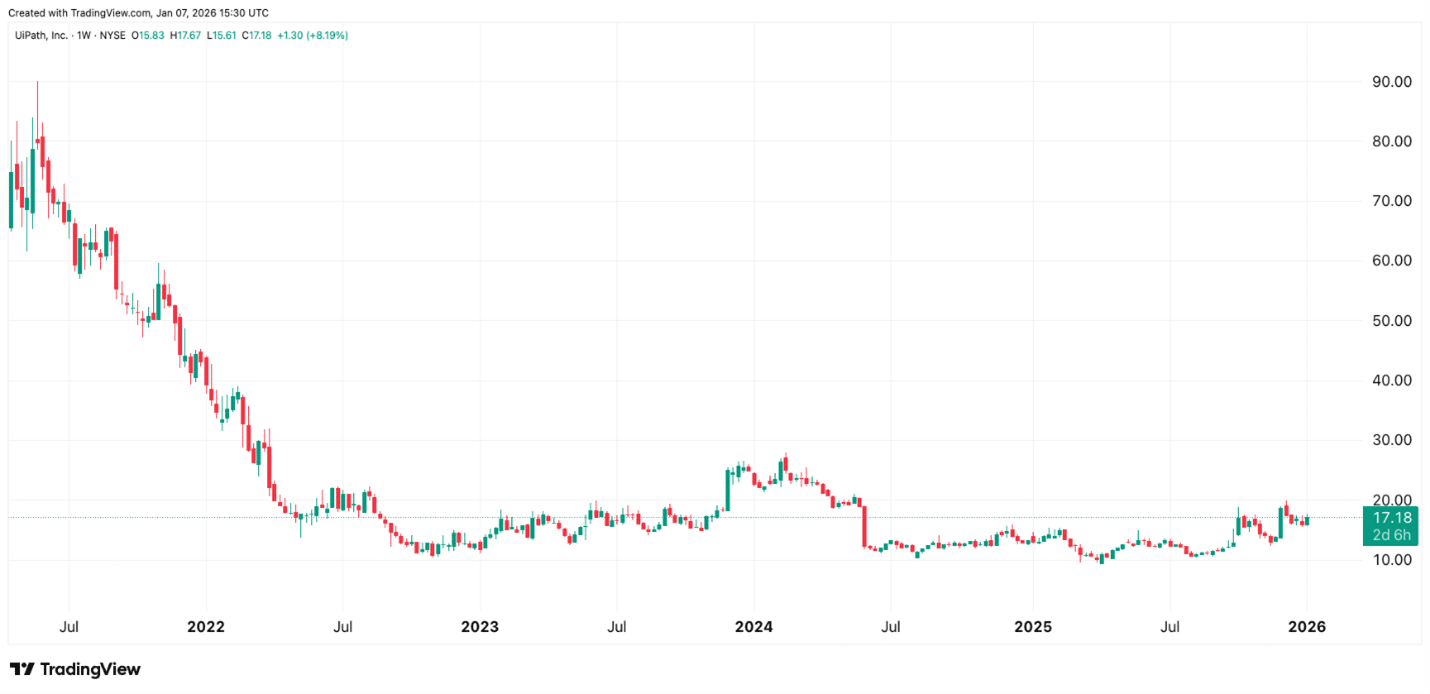

NYSE: PATH – $16.88 per share as of market close on January 8th

Challenges Since the 2021 IPO – UiPath’s Underperformance

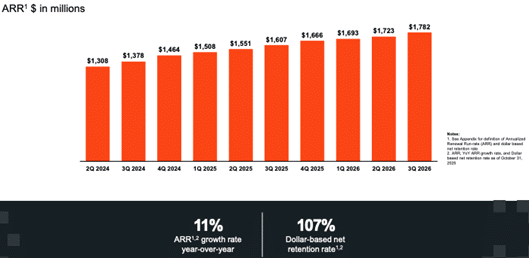

- Top line growth rates slowed significantly since going public. ARR growth decelerated from 65% in Q1 FY2022 to 11% year over year during the Q3 FY2026 quarter.

- Competition intensified in the RPA market. Major tech companies such as Microsoft and Salesforce offering similar automation tools, creating pressure on margins.

- The rapid emergence of AI and LLMs created angst amongst investors that RPA could be disrupted and become obsolete. This narrative weighed on investor sentiment and caused significant volatility and valuation multiple compression in UiPath’s stock.

- Dollar based Net Retention Ratio (NRR) remains expansionary at 107%, indicating that existing customers are increasing spend. Notably, the NRR on contracts between $100,000 and $1 million was 113%, indicating that the larger contracts are outperforming the lower end of the market.

- Customer related metrics are rebounding: Total customers reached 10,860 (up 12% year-over-year), and the gross retention ratio was 98%, demonstrating customer stickiness. Net new ARR has trended upwards sequentially during the first three quarters of FY2026, and Q4 guidance suggests further growth is anticipated. This indicates that sales execution and product demand are strengthening.

- Q3 FY2026 delivered beats over analyst consensus on Revenue and EPS, and management issued strong guidance for Q4. It was the first profitable Q3 for UiPath in its history, and the company signalled it is on track for a full fiscal year of GAAP profitability.

- Several key partnerships were announced in 2025, including with OpenAI, Microsoft, Google, Snowflake, and Nvidia, providing strong validation of UiPath within the enterprise AI stack.

Maestro – The Key to Growth Acceleration

The pricing structure of Maestro has not yet been disclosed, but Daniel Dines has stated that they are exploring outcome-based pricing, consistent with the approach taken by Palantir. This is a strong indicator of confidence in the product’s potential.

Customer Use Cases

To provide an idea of the real-world impact Maestro is delivering, here are a few standout examples that were discussed on the Q3 earnings call:

- USI insurance, one of the largest Insurance brokerages in the world uses Maestro to process incoming requests and generate output. “USI expects over $32 million in savings over the next 3 years.” – Daniel Dines on the Q3 earnings call.

- One of the world’s largest investment management firms is also a Maestro client, integrating it with ServiceNow, Confluence and specialized LLMs to orchestrate end-to-end workflows. Maestro has delivered a “95% reduction in time to value and tens of millions in projected savings” according to Dines.

- Other customer use cases discussed on the earnings call include the U.S. Federal Government, Corewell Health, Energie, and the U.S. Coast Guard.

The industries mentioned (insurance, financial services, healthcare, and government) are among the largest industries in the world. Even if UiPath can rollout Maestro among its existing customer base, the revenue growth potential is huge.

Valuation – Asymmetric Risk/Reward Characteristics

UiPath trades at a forward non-GAAP P/E of 25x, P/CFO of 24x, and an ARR multiple of 5x.

For a growing and profitable software firm with strong tailwinds from AI, these multiples appear undervalued relative to peers such as Snowflake, Palantir, ServiceNow, and Appian. The balance sheet is clean, with 1.4B in cash and equivalents and no material debt. In my opinion, the current share price and fundamentals provide a significant margin of safety, limiting the downside if growth does not accelerate as forecasted. After studying the impact that AI is having on the business and the product roadmap, I am confident that UiPath’s accelerating top line growth could surprise the market in 2026, triggering a significant rerate in the valuation and share price. The market still seems to be pricing UiPath like it is an aging RPA business and has not yet fully reflected the agentic AI / Maestro opportunity.

Founder Led Company

When analyzing any company, the management team is one of the most critical factors to assess. UIPath scores highly with its founder & CEO, Daniel Dines. Dines is a Romanian software engineer with a master’s degree in mathematics and computer science from the University of Bucharest. He began working at Microsoft in Seattle from 2001- 2005 before leaving to start his own company, DeskOver, which eventually renamed to UiPath. Since founding the company 20 years ago, Daniel has grown UiPath from humble beginnings in Bucharest to the $9B company that it is today.

Daniel Dines briefly stepped aside in January 2024 and Rob Enslin was appointed CEO. This was a turbulent time for UiPath as it faced declining growth rates, competitive pressures, and threats from AI. During Rob Enslins brief term as CEO, UiPath reported weakening quarterly results that missed guidance estimates, with management citing a longer sales cycle and lower average deal sizes. Investors grew increasingly concerned about the future of UiPath, Rob Enslin resigned, and Dines returned as CEO in June 2024 with a renewed focus on profitable growth, and product innovation.

After watching hours of his interviews, presentations, and earnings calls, I have confidence in Daniel as a CEO to keep the company on the right track and deliver strong shareholder returns.

Daniel Dines – Founder and CEO of UiPath

DISCLAIMER

* Not financial advice, do your own research. Torrent is long shares of PATH through shares and/or options. This article expresses the author’s own opinions and there is no business relationship with any company whose stock is mentioned in this article. No recommendation or advice is being given as to whether any investment is suitable for a particular investor.